Implications of new growth phase in Australian impact investing

Impact investing in Australia has reached a significant milestone with a leading superannuation fund committing $30m to impact investment through a dedicated trust managed by Social Ventures Australia (SVA). Alex Oppes looks at what this means for impact investing in Australia.

- Charities and social sector

- Housing and homelessness

14 min read

14 min read

- How the milestone $30m commitment from a leading superannuation fund heralds a new growth phase for the Australian impact investment market.

- What the next generation of large-scale impact investing opportunities is likely to look like.

- How and why the investor interest in impact investment has changed.

The announcement of a partnership between HESTA and SVA with the launch of a $30m Social Impact Investment Trust represents a coming of age for impact investing in Australia. The Trust is the largest Australian impact investing commitment made by a superannuation fund. This article explores why this is a significant moment for the development of the impact investment market and explains what this means for investors and for the social sector.

Key facts: The Social Impact Investment Trust

- Size: $30m

- Target deal size: $1-10m

- Asset classes: Debt/equity/social impact bonds

- Target impact areas: Social and affordable housing, social sector organisations, social businesses, social impact bonds

- Target returns: To be determined on a deal by deal basis, based on the risk of the investment

- Investor: HESTA, the industry fund dedicated to Australia’s health and community services sector, with more than $32 billion in total assets and over 800,000 members.

- Manager: SVA, a non-profit organisation that works to improve the lives of those in need. SVA offers impact investing, advisory and funding services.

Impact investing market enters growth stage

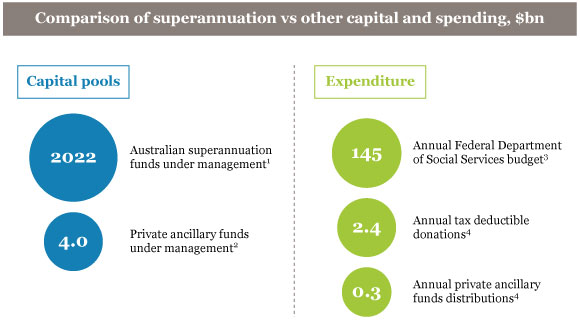

For years, the social sector has had limited access to potential investment capital from Australia’s superannuation industry. At $2.05 trillion in size,[1] Australia’s superannuation industry is the world’s fourth largest pool of retirement savings,[2] approximately 500 times larger than Australia’s total private ancillary fund corpus[3] and significant in comparison to private philanthropic giving and government expenditure on social services.

- APRA, Quarterly Superannuation Performance June 2015

- JB Were, The PAF Report, December 2014

- Commonwealth Government, Portfolio Budgets Statements 2015-16

- JB Were, Australian Giving Trends, August 2014

- JB Were, The PAF Report, December 2014

To be clear, superannuation will never replace government expenditure on social services, nor the vital role of donors, but it can supplement these sources in order to offer a broader array of funding options to non-profit organisations and social enterprises, as well as support the growing social impact bond market. And if only a small percentage of Australia’s superannuation capital can be deployed constructively into the social sector, the impact could be tremendous.

Yet up until now, superannuation funds have invested very little into Australian impact investing projects. Notable superannuation investments have included NGS Super’s investment in the Newpin Social Benefit Bond[4], Christian Super’s investment in the Newpin Social Benefit Bond[5] and Foresters’ Social Enterprise and Development Investment Fund (SEDIF)[6], and Good Super’s investment into SVA’s SEDIF Fund.

Michael Traill, founding CEO of SVA, reflects on the early engagement of superannuation funds with the SEDIF Funds and social impact bonds.

“While we all recognised getting substantial super fund commitment to impact investing would take time, the fact that some funds started to put a toe in the water with small investments was a bellwether of what was to come,” says Traill.

“We have moved a long way since our early social enterprise investment deals like Bonsai Social Firm in 2006, when we would not have contemplated going to major institutional investors like the super funds.”

HESTA’s commitment therefore represents a milestone in terms of size, source and social commitment. It is the first large-scale investment by a top 10 Australian superannuation fund.[7] The fund is also notable for a number of innovations, in particular its impact-based incentive structure. Under the terms of the fund, the management compensation structure incorporates both a financial and a social hurdle (compared with a typical private equity or venture capital fee structure that incorporates only a financial hurdle).

This means that the investor and manager agree upfront on social targets and the manager is incentivised to achieve the blended social and financial returns. A robust impact assessment methodology, based on the Global Impact Investment Network’s Impact Reporting and Investment Standards, will be used to track social impact.

…the commitment from HESTA is a clear signal to the mainstream market that there are opportunities appropriate for institutional investors that create positive impact for our communities.

The start of large-scale investment by superannuation funds arguably heralds a new phase for the Australian impact investing market. Impact investing is moving from the pioneering phase to a growth phase, one which will look different in terms of its investors, transactions and intermediaries. On the investor side, the movement by a leading superannuation fund is likely to send a signal of confidence to the rest of market and may result in ‘crowding in’ by other institutional investors. SVA is actively seeking similar partnerships with other investors, with the aim of raising $100 million in funds under management over the next 12 months.

Chair of Impact Investing Australia, Rosemary Addis explains, “This is an exciting development for the Australian market; the commitment from HESTA is a clear signal to the mainstream market that there are opportunities appropriate for institutional investors that create positive impact for our communities.”

The growth stage is also likely to see an increasing number of transactions at scale and growth of an eco-system of intermediaries to support the development of social enterprises and projects from idea stage through to investment readiness.

The implications of this transition from pioneering to growth stage will be explored in the remainder of this article.

| Phase | Investors | Transactions | Intermediaries |

|---|---|---|---|

| Pioneering phase | – Private wholesale investors as early adopters (including high net worth individuals, private ancillary funds (PAFs), self-managed super funds (SMSFs)) – Relatively high degree of uncertainty (Government support typically required) | – Small scale pilot transactions with early-stage social enterprises (often without real property assets) and larger social sector organisations trialling social enterprise – Large range of impact areas | – Establishment of market infrastructure (intermediaries, specialisations, methodology and language) – Focus on capacity building, developing market awareness, trialling broad portfolio of pilot transactions |

| Growth phase | – Larger scale commitments by leading institutional investors and ethically-focused institutional investors – Increasing acceptance of impact investment as a standard asset class within investment portfolios | – Increasing number and size of transactions, building on successes and lessons from pioneering phase investments – Increasing focus on measuring impact on key societal issues | – Increasing in number of intermediaries, degree of specialisation and new product offerings – Increasing interest from mainstream financial intermediaries |

| Maturity phase | – Investors increasingly applying impact criteria across entire portfolio – Ability to invest in range of impact investing asset classes (property, equity, debt) – Direct participation by retail investors (‘mums and dads’) | – Execution of wide range of transactions providing risk/return and impact profiles to suit all investors (from ‘impact first’ to ‘finance first’) – Increasing number of ‘at scale’ transactions (>$20m) | – Broadening array of mainstream financial services firms and specialised intermediaries – Increasing competition between intermediaries based on track record and offering – Ongoing innovation, including introduction of secondary markets |

Building the pipeline of large-scale transactions

An effective social sector requires different types of capital for different purposes. Many programs require grant funding because returnable capital, like debt or preferred equity, is typically not appropriate for early stage social enterprises with modest revenue. At the next stage of investment opportunities, funds like the SEDIF Funds can invest in social enterprises seeking relatively small-scale growth capital. At the larger scale, the backing of superannuation funds gives the social sector access to finance to tackle some of society’s biggest issues in a meaningful way, including aged care, disability, employment, housing and indigenous issues.

Investment-ready opportunities

One of the main barriers to the development of the impact investing market to date has been around the relative scarcity of large-scale, investment-ready opportunities. In Australia to date, the SEDIF Funds have collectively committed just over half of their funds available. Similarly in the UK, scale has been somewhat problematic in the early years of the market and Big Society Capital and its co-investors have so far drawn down only £104m of the £359m available to invest.[8]

… Australia will need to focus on investment readiness at a much larger scale.

Many large-scale social issues don’t have obvious, economically viable solutions. Instead, creative solutions are often required, and these take time, expertise and funding to develop. Providing appropriate support to earlier stage organisations in Australia will be key to helping them access the finance that is available. Accelerators such as the School for Social Entrepreneurs and Social Traders play an important role nurturing early stage organisations in Australia, whilst venture philanthropy and more recent initiatives, such as NAB’s $1m Impact Investment Readiness Fund, provide the funding for early-stage organisations to access professional services necessary to become investment ready.

In order to capture the full impact investment opportunity, Australia will need to focus on investment readiness at a much larger scale.

The UK is leading the way with its investment readiness programs. One highly successful government policy in this area has been the UK Government’s Investment and Contract Readiness Fund (ICRF). This Government grant program supported social ventures to build their capacity to be able to receive investment and bid for public service contracts. The ICRF helped social sector organisations acquire the strategic, finance and legal skills they needed to raise investment and compete for public service contracts. In a 2014 review of the ICRF program, Boston Consulting Group found that ‘for every £1 spent by government, £43 has been raised through additional investment or contract values’ and noted that ‘in one deal alone, Empower Community Management raised over £10m in investment’.[9]

More recently, the UK Cabinet Office, Big Society Capital and Big Lottery Fund have jointly established the Access Foundation, a £100m foundation aimed at helping early stage social enterprises and charities access finance. The Access Foundation will deliver support via a Growth Fund (providing matched loan and grant capital up to £150,000) and its capacity building programmes.[10]

Areas to watch

Despite the lack of large-scale investment readiness programs in Australia, we are starting to see the gradual emergence of more opportunities at scale, notably in the areas of social and affordable housing, ‘take social’ opportunities, social procurement and social impact bonds.

1. Social and affordable housing

In the area of housing, there are approximately 160,000 Australians currently on public housing waiting lists.[11] We need to start looking at ways to enable large-scale construction of new social and affordable housing that can reduce waiting lists.

Two innovative approaches to social housing in Australia are the Bonnyrigg Living Communities Project and the recent Sustain Community Housing development. The Bonnyrigg project was Australia’s first public-private partnership in the area of social housing, revitalising an 81 hectare, 2400 dwelling housing estate in western Sydney. This $368m project covered the financing, planning, developing, designing, construction, refurbishment and maintenance of public housing.[12]

Innovative developers and community housing providers are also working on transactions that do not rely on government. For instance, the $2m pilot-scale deal between Sustain Community Housing, SVA and Social Enterprise Finance Australia (SEFA) will trial an innovative model for social and affordable housing – the mixed development. In what is expected to be the first development of many, six dwellings are being built on subdivided land in Colyton in western Sydney. Four of these dwellings have been sold privately to cover the cost of the project and two dwellings will become social housing which will be retained by Sustain Community Housing.[13] These social and affordable housing transactions increasingly offer the potential for large-scale impact investing transactions.

2. ‘Take social’ opportunities

‘Take social’ transactions range from investments in for-profit businesses with the capacity to create significant social impact (such as SVA’s investment in PGM Refiners, a business with a commitment to employ a minimum of 70 per cent of its operational staff from long term unemployed backgrounds) to distressed asset buyouts of private businesses with the potential to create social impact (such as GoodStart).

The 2009 GoodStart transaction remains one of the largest impact investment transactions globally, involving the rescue of the ABC Learning business by a non-profit syndicate. The transaction required $165m of layered finance, involved over 40 investors and continues to impact the lives of over 70,000 children.

Meanwhile, the 2015 sale of Home Care by the NSW Government is a more recent example of large-scale impact transactions. Home Care has a 70 per cent market share in NSW, helping older people and people with disability to live independently in their own homes as well as providing support to carers.[14] The $114m bid for the government business by the mutual Australian Unity is expected to be finalised in early 2016 and illustrates the potential for new models of service delivery in Australia.[15]

GoodStart: At a glance[16]

- Description: Buyout of 678 ABC Learning centres from voluntary liquidation and establishment of new, non-profit entity

- Transaction size: $165m

- Number of investors: 41 impact investors, NAB, Australian Government and non-profit syndicate members

- Social Impact: Improved quality of early childhood education for 73,000 children

3. Social procurement

Social procurement contracts are typically issued by either government or corporates, and include consideration of social factors – such as employment of disadvantaged groups – in the tendering process. In Australia, the Commonwealth Government has committed to place 3 per cent of its procurement contracts with Indigenous suppliers by 2020 – an estimated 1500 contracts or $135m each year.[17] This will create large working capital needs – and hence impact investing opportunities – for winning bidders. Yet the social procurement opportunity is much broader – it is an opportunity at all levels of government and in the corporate world.

In the UK for instance, the Social Value Act is a relatively new law that requires that commissioners of public services consider social impact factors in tendering processes – and not just focus on price.[18] Social procurement in the UK has fuelled the growth of social enterprise champions such as the HCT Group, a social enterprise that operates many of London’s red buses, providing 20 million passenger trips every year.[19]

4. Social impact bonds

Social impact bonds (SIBs) represent an emerging financing area for social impact investing. SIBs reflect a new approach to government procurement, where governments pay service providers where they achieve a set of social ‘outcomes’, rather than just on the traditional ‘outputs’ basis. Social impact bonds typically finance preventive and early intervention services that tackle social issues that generate long term savings for government. The structure allows for a sharing of risk between the government, service providers and private investors.

There is a growing recognition across all levels of governments that to effectively tackle some of Australia’s costliest problems… innovative larger-scale interventions are required…

Two social impact bonds have been created to date, both in NSW. However, several States and the Federal Government have recently expressed intention of piloting new social impact bonds. In South Australia, the government has recently announced that it will proceed to negotiate with local homelessness service providers, Hutt Street Centre and Common Ground Adelaide, to develop South Australia¹s first social impact bond with the support of SVA.[20]

The Queensland Government has recently announced a social impact bond pilot program,[21] whilst the NSW Government has committed to a further two social impact transactions per year.[22] The Federal Government has signalled a desire to explore intervention and prevention initiatives funded by social impact bonds as a means of reducing the Government’s $150bn social services budget. There is a growing recognition across all levels of governments that to effectively tackle some of Australia’s costliest problems, such as chronic health care issues and youth unemployment, innovative larger-scale interventions are required, suggesting that larger social impact bond transactions may be on their way.

Growing investor interest in impact investing

What has changed?

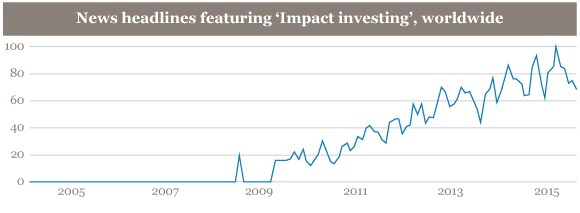

Why has it taken until now for the superannuation industry to commit capital to impact investing? Several notable factors have changed recently. First, and perhaps most importantly, there has been a rapid increase in public awareness of impact investing.

Whereas ethical investing[23] has been popular amongst investors for decades, the idea of impact investing – using investment to intentionally create positive social impact alongside a financial return – has only recently captured mainstream attention and headlines in Australia. Up until now, impact investing opportunities have been mainly limited to ‘wholesale investors’ in order to comply with onerous ASIC product disclosure requirements.[24]

…the impact investment landscape presents an opportunity to identify investments that are aligned with our members’ values…

It is now possible for mainstream Australia to access impact investment opportunities simply by being a member of certain superannuation funds, which in turn allocate a percentage of their portfolios to impact investing. In the case of HESTA – the industry fund for the health and community services sector – the alignment with members’ interests is clear.

Robert Fowler, HESTA’s Chief Investment Officer, says that “We have had strong support from members to invest in this area, therefore, the impact investment landscape presents an opportunity to identify investments that are aligned with our members’ values, as well as to engage in helping build the impact investment market in Australia.”

The second factor that has changed for impact investing is the development of an industry track record in the last few years, which has given innovative institutional investors the confidence to invest in a relatively new asset class. Key players in developing this track record include the pioneering early investors in the space, government (including the Federal Government’s SEDIF program and NSW Government’s two social impact bonds) and intermediaries.

The SEDIF track record, in particular, has been instructive. The three fund managers, SVA, Foresters and SEFA, have collectively committed nearly $20m of funding to more than 50 impact investments. These investments span a wide range of asset classes (from debt to equity) and impact areas. Collectively, we now have a better understanding of what works in impact investing – and what doesn’t – and laid the foundation for larger scale investments.

… we identified that the most effective way to evaluate and source investments was through a partnership approach… with a group dedicated to assessing impact investment with similar social impact goals.

Fowler notes that “Over the last 12 months, our Investment Strategy team spent time researching the Australian impact investment market by reviewing historical transactions, meeting with Australian intermediaries involved in promoting impact investment strategies, and discussing impact investment trends with international groups.

“As a result, we identified that the most effective way to evaluate and source investments was through a partnership approach – in the same way to how we work with other managers in HESTA’s investment portfolio – with a group dedicated to assessing impact investment with similar social impact goals.”

The emerging industry track record in impact investing is helping to overcome one of the key hurdles for institutional investors in impact investing – the sole purpose test. Trustees of superannuation funds are under a fiduciary requirement to invest for the ‘sole purpose’ of providing retirement benefits for members.[25] In Australia it is therefore clear that impact investing must meet financial benchmarks commensurate with mainstream investments. The emerging impact investing track record established over recent years is providing comfort that solid risk adjusted returns can be achieved.

Fowler notes that achieving an appropriate financial return alongside measurable social impact was a crucial to investing in the sector. “We have a fiduciary duty to ensure we are acting in the best interests of our members. Therefore, appropriate return and risk characteristics are essential within the investment framework and evaluating prospective impact investments. HESTA and SVA will seek to implement a highly selective approach, focusing on investments that we believe have the potential to achieve financial net returns consistent with HESTA’s return expectations for the relevant type of investment.”

The second benefit from a fund manager perspective is the opportunity to diversify.

Some impact investments can offer appropriate risk-adjusted returns and diversification benefits. Impact investing includes sectors of the economy such as ageing and disability that are forecast to grow rapidly relative to the rest of the Australian economy over coming years. Sectors such as disability have not traditionally been mainstream investment targets, but with the introduction of the National Disability Insurance Scheme, these areas are set to grow rapidly.

Superannuation funds will therefore be able to gain exposure to these growing sectors of the Australian economy, as well as ensure measurable social positive outcomes through impact investment portfolios and specialist intermediaries that understand these markets. The second benefit from a fund manager perspective is the opportunity to diversify. Impact investment is an asset class that is arguably less than perfectly correlated with other asset classes. In the area of social impact bonds, for instance, returns are dependent on social outcomes achieved and are likely to have lower correlation than investments with traditional business-cycle driven investments.[26]

Where to from here?

Superannuation funds are increasingly interested in social and environmental investment, but government could increase the speed and impact of this. Governments can potentially save money overall by providing financial incentives to support impact investment. Successful impact investments result in positive externalities – such as job creation for long term unemployed people, better quality of life for people with a disability, and a reduction of public housing waiting lists. Many of those positive impacts result in savings to government. In the same way that the government taxes activities that result in negative externalities (such as smoking), the government can encourage activities that result in positive outcomes to society, either through tax relief or direct government outlays.

Several submissions to the Australian Government’s Tax White Paper Public Consultation proposed such incentives, based on successful overseas schemes.[27] The UK introduced Social Investment Tax Relief in 2014, allowing investors to claim a reduction of 30% of their qualifying impact investment from their taxable income in the year of investment.[28] This incentive has helped catalyse new tax-effective impact investments and funds such as the Resonance Bristol Social Investment Tax Relief Fund launched in August 2015.[29] A similar scheme has been established in the US via the Federal New Markets Tax Credits and the Community Reinvestment Act. Both of these US programs are designed to increase the flow of capital to low socio-economic areas, and since 2000 over $43.5 billion in new market tax credit transactions have been approved.[30]

Conclusion

HESTA’s capital commitment paves the way for catalytic growth in the Australian impact investing market. Engagement from one of Australia’s largest superannuation funds sends a strong message of confidence about the potential for impact investing in Australia and builds the profile of the sector.

This commitment by HESTA provides part of the puzzle in the social sector eco-system. Developing a pipeline of scale-appropriate, high-impact opportunities and furthering the investment readiness of the social sector is now the challenge ahead.

Author: Alex Oppes

[1] APRA, Quarterly Superannuation Performance, June 2015. APRA website, accessed Oct 2024

[2] Towers Watson, Global Pensions Assets Study 2015,

[3] JB Were, The PAF Report, December 2014.

[5] Christian Super website

[6] Kylie Charlton, Scott Donald, Jarrod Ormiston and Richard Seymour, Impact Investments: Perspectives For Australian Superannuation Funds, 2013

[7] Sydney Morning Herald, Hesta dumps transfield citing detention centre abuses, 18 Aug 2015, accessed Oct 2024

[8] Big Society Capital, 2014 Annual Report, Big Society Capital website, accessed Oct 2024

[9] Boston Consulting Group, Ready, willing and able: an interim review of the Investment and Contract Readiness Fund, 2014, BCG website, accessed Oct 2024

[10] Access Foundation website

[11] Australian Government, Reform of the Federation White Paper: Roles and Responsibilities in Housing andHomelessness, page 20

[12] NSW Treasury website

[13] SVA website, Impact investment to fund affordable housing, April 2015

[14] NSW Government, Media release: $100m to be reinvested in disability services after NDIS milestone, NSW Treasury website, 2015, accessed Oct 2024

[15] Herbert Smith Freehills website

[16] SVA, GoodStart: a social investment story, 2019

[17] Minister for Indigenous Affairs, Senator the Hon Nigel Scullion, Media release: Minister Scullion: Commonwealth taking steps to increase Indigenous jobs, Indiginous.gov.au, 17 March 2015, accessed Oct 2024

[18] UK Government, Social Value Act: information and resources

[19] HCT Group website

[20] South Australian Government, Media release, 27 August 2015

[21] Queensland Government, Media release, 12 July 2015

[22] NSW Treasury, Social Impact Investment Policy, NSW Government website

[23] Typically involves the use of positive or negative ethical screens to rule in or out investments

[24] Such as high net worth individuals, private ancillary funds (PAFs), self-managed super funds (SMSFs) and trusts and foundations, as defined in section 761G of the Corporations Act 2001 (Cth). Under the Corporations Act, higher levels of disclosure are required when offering investment products to retail investors.

[25] Superannuation Industry (Supervision) Act 1993

[26] UK Social Impact Investment Taskforce, Allocating for Impact: Subject Paper of the Asset Allocation Working Group, 2014.

[27] Pro Bono News, Call for Tax Concessions for Impact Investments, 2015, accessed Oct 2024

[28] HM Revenue & Customs and HM Treasury

[29] Resonance Bristol SITR Fund Information Memorandum, 2015,

[30] CDFI Fund, ‘New Markets Tax Credit Program’